US Stock Markets rallied past week to all time highs and stocks on Wall Street have soared to fresh record highs, but it’s not because the economy is flashing a big thumbs-up sign. It’s not. The economy is still expanding, to be sure, and sporadic worries about recession have faded again. Yet U.S. economic growth has slowed sharply from earlier in the year and there’s little reason to expect a holiday-season bonanza for the economy.More evidence of a slowdown emerged in a pair of recent reports on industrial production and retail sales — windows into how businesses and consumers are faring. In the meantime the worldwide debt has been soaring above 250.000 billion…. This headline in the Belgian Financial Newspaper De Tijd did catch my attention.

The Institute of International Finance (IIF) said there are no signs of slower growth and sees the worldwide debt take the peak of 255.000 billion. That is 3 times the debt that world owned in 1999. The US government and China account for the biggest growth. They are responsible for 60% of the growth. IIF notices that more than half of the new debt growth is owned by government companies. If they get in trouble, governments will own the troubles.

In order to stimulate the economic growth, central banks continue to create new money through quantitative easing. The Fed now also started to lower interest rates again after pressure of President Trump. But should they?

In a column of PBS in June 2016, the Harvard economist Terry Burnham and economics correspondent Paul Solman explore two different views in two separate pieces. Terry Burnham warns against quantitative easing. You can also read Paul’s take on the issue at the following link, “Why the Fed should print more money, not less,” here.

The Blackstone Group Inc. (BX), one of the world’s largest private equity firms with $554 billion in total assets under management, sees growing risks for the markets right now, including a largely overlooked “mother of all bubbles.” Moreover, there actually are troubling linkages between several negative developments that, on the surface, appear to be random and unrelated, warns Joseph Zidle, chief investment strategist at Blackstone’s private wealth solutions group, per a detailed Business Insider report that is summarized below.

“The failures in the repo market, negative-yielding debt, a deeply negative term premium, trade conflicts around the world and a collapse in manufacturing all seem unrelated right now, but I don’t think they are random,” Zidle wrote in a recent note to clients. His biggest concern is negative yields on sovereign debt worth $13 trillion, what he believes may be “the mother of all bubbles.”

KEY TAKEAWAYS

- Seemingly unrelated risks produced the 2008 financial crisis.

- Today, various apparently random events actually are linked.

- Their combined negative impacts are potentially massive.

- Negative interest rates on sovereign debt may be the biggest bubble.

What is Significance For Investors

Zidle sees a troubling parallel with the 2008 financial crisis, which erupted after a number of apparently unrelated risks converged. Meanwhile, CEO Steve Schwarzman of Blackstone searches for “discordant notes,” or trends in the economy and the markets that appear to be separate and isolated, but which can combine with devastating results. Zidle sees negative yields on sovereign debt as the loudest discordant note today. Heavy speculation in such debt is producing massive price swings, at odds with the traditional stability that fixed income securities give to investment portfolios. For example, a 100-year bond issued by Austria doubled in price within 2 years. Schwarzman has similar concerns about interest rate cuts by the Federal Reserve. “Interest rates are historically low in the United States, and you keep driving them lower, where do you get? What’s the objective?” he asked rhetorically during a recent interview with MarketWatch. “If you push down [interest rates] too much, you create the problem you are trying to solve,” he continued, indicating that low rates are hampering economic growth, in his opinion. Schwarzman also worries about slowing economic growth and rising numbers of IPOs from loss-making companies. As recently as 2018, he notes, the world economy still enjoyed largely synchronized growth. Now most countries are in slowdowns. He calls IPOs from unprofitable companies “signs of excess” that often accompany the late stages of an economic expansion. Indeed, large numbers of unprofitable companies going public also marked the dotcom bubble, per a report in Bloomberg.

Harris Kupperman, president of Praetorian Capital Management and CEO of Mongolian Growth Group, has similar concerns. “When you push liquidity through the system like they [the Fed] have the last ten years, you create a giant bubble,” he told BI in an earlier report. “I’ve been through 2 crashes in my life, and I think this is the third one,” he added. Kupperman also blames the Fed for creating a “Ponzi sector,” which includes “companies that have no chance of ever earning a profit,” but which attract investors.

Meanwhile, mortgage backed securities (MBS), whose cratering values were a key catalyst for the 2008 crisis, today are in vicious cycle called negative convexity. Falling interest rates are causing their prices to decline rather than rise, as described in another BI article.

Another contributor to the 2008 crisis was inflated corporate bond ratings, and that problem persists today, The Wall Street Journal reports. Additionally, high risk leveraged loans have been collapsing in value, and the total global exposure may be as high as $3.2 trillion, per the Bank of England (BoE).

The End Conclusion : the monetary bubble to end all bubbles

Given these alternatives, the most likely outcome is financial crisis. As the crisis unfolds, we should expect people to claim, “NEVER AGAIN.” You can get ahead of the crowd. Say it now. “Monetary policy cannot make us rich; we will never again try to print ourselves to prosperity.” Open the window and scream it:

“NEVER, NEVER, NEVER again.” And then hope you die before the next round of monetary printing. Many elderly Germans who lived through the 1930s cannot believe the current situation. They are mad as hell, but there are too few of them alive to alter the outcome. The seed of future monetary shenanigans grows with each funeral of people who lived through the prior crises.

Zidle, chief investment strategist at Blackstone’s Group, believes that the current biggest problem is trade. In his opinion, solving this issue would boost business confidence, keep job growth strong, and extend the economic expansion. Given the current macro environment, he does not expect a recession within the next 6 months, but he thinks that the current expansion is unlikely to persist for more than 2 years. Enjoy riding the longest bull trend in human history.

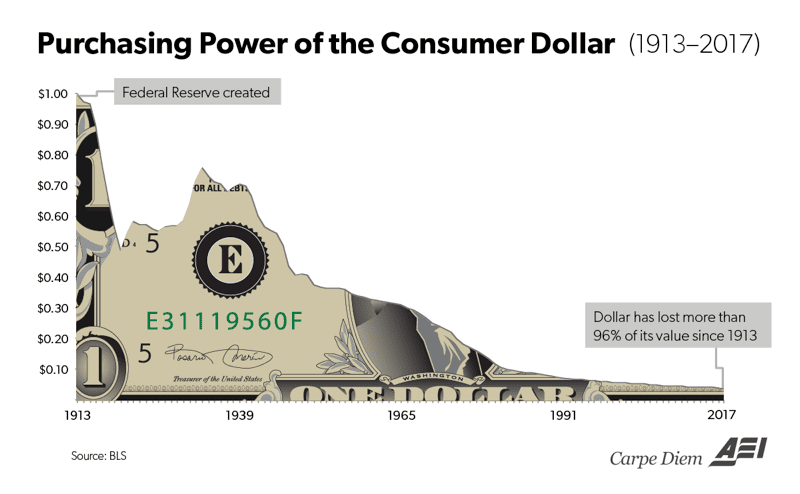

Gold and Silver did their corrections and wait for crash confirmation signal before starting to pump as investors realize that they must save their wealth and they need to start buying Gold and Silver in order to do so. You should already be familiar with the dollar lost in it’s buying power through years and it’s unlimited supply, it fells 98% from it’s first issuance as we saw it on a picture below.

Will gold and silver be the only way to save your wealth or is there new place to store your fortune like bitcoin? We will see. But the fact is that the crash is imminent and inevitable. Stay safe and do your own research. This is NOT a financial advice.

This is the end of this blog post.

In 2019 we will send out ONE newsletter per month to our blog followers. Life can be busy sometimes and people lose track of following a personal finance and travel blog. Subscribe and you will get one email per month highlighting what you missed…

Thanks for following us on Twitter and Facebook and reading this blog post. We end with a quote as always.

No Comment

You can post first response comment.