In the week of the 27 – 31st of March, the week of the Money started to educate kids (and adults) personal finance. The goal was also to place personal finance more in the picture.

You can read more information on the following URL : http://www.deweekvanhetgeld.be

On Monday 27th, a press release of Wikifin.be was released with the results of a large savings survey conducted in Belgium. In this blog post, we will summarize the findings of this survey, discuss risk management in general, and reflect with some conclusions.

1. Results of the savings survey

More than 1000 Belgians between 25 and 74 were interviewed about their savings behavior. Here are the main conclusions :

- 67% of Belgians are saving money. 33% did NOT during the past 12 months

- 25-34 year old are saving more. 35-44 year old and 65+ saved less than the past 12 months

- People with a higher education save more

- 47% of the saving people have a negative feeling about it as they feel frustrated because they can’t save more or spend too much money

- One out of 5 Belgians that couldn’t save, didn’t have the means to do so. But also people didn’t save because they say they lose money anyways…it doesn’t give any return…

- On average people save 186 Euro per month.

- 43% saves every month. 24% saves less frequently

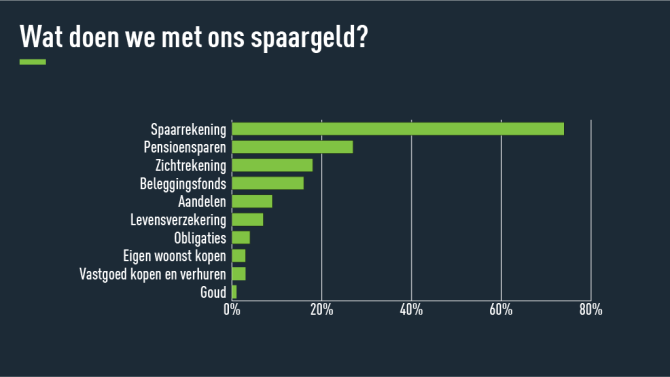

- What does the Belgian do with his savings ? See the graph. More than 70% puts it on a savingsaccount. 15% puts it on their normal account…

- 40% of Belgians think they have enough savings. 44% believes they do NOT. 8% does not have any savings.

- 28% believe their savings did increase. 33% believe it decreased. The reason for decreasing savings was higher expenses, and unexpected costs.

- What did impact the savings behavior ? The low interest rate, and feeling about an unsecure future are the main reasons. 15% prefers to enjoy life and spend money

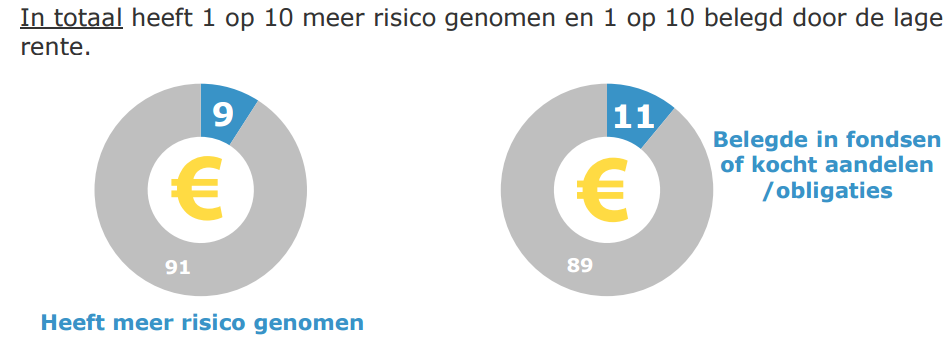

- ONLY 1 % did take more risk to invest their money and purchased funds or stocks

You can find the DUTCH version of the results here : onderzoekmaart17

So what are the key insights we take forward from this survey :

- Belgians keep on saving and the low interest rates don’t stop them. One out of 3 Savers think the interest rate is between 0,16% and 9,99%…

- They mainly put it on a savings account for unexpected costs and building their wealth. Average value is 186 Euro.

- Only 1% has appetite to invest his money in the stock market and does take risk.

We will review and discuss now why risk management is important. We think Belgians need a course in RISK MANAGEMENT

2. What is Risk Management ?

According to Wikipedia, Risk management is the identification, assessment, and prioritization of risks followed by coordinated and economica l application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities. Risk management’s objective is to assure uncertainty does not deflect the endeavor from the business goals. Risks can come from various sources including uncertainty in financial markets.

l application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities. Risk management’s objective is to assure uncertainty does not deflect the endeavor from the business goals. Risks can come from various sources including uncertainty in financial markets.

Now let’s make an analogy for putting risk management in perspective. We believe everyone wants to learn how to drive a car, right? We also believe that everyone would love to learn how to grow your money.

So let’s put those two things next to each other in a table…

| Driving a car |

Investing in the stock market |

|

|

Objective |

To take you from point A to point B | To grow your money |

|

What do you need? |

A Driver’s license, investment in driving courses, investment in a (second hand) car, Insurance | Invest in financial courses, books on how to invest and select funds, stocks, ETF’s. Read my blog and other bloggers. Watch YouTube videos |

|

What are the risks involved? |

||

|

Identify the risks |

1. Driving knowledge: knowledge how to drive a car, learn the road signs and code.

2. Car accident 3. Car damage due to weather, violence, other. 4. Theft 5. Maintenance: flat tire, engine issues, other. |

1. Investment knowledge: learn what to invest in that gives you money. Learn about dividend investing as example

2. Identify online brokers to lower your purchase costs 3. What is your risk level? If you lose 5% of your money, how would you feel? |

|

Assess the risks |

You assess all the risks involved and take action to mitigate the risk | You assess all the risks involved and take action to mitigate the risk |

|

Control and avoid the risks |

1. You take courses to learn how to drive, learn the road rules and code

2. You purchase a car insurance 3. You go for maintenance to a car dealer on a frequent basis.

|

1. You only use 10% of your money for each stock or ETF you want to purchase. This is diversification. You invest in your knowledge on how to select and find those value qualitative stocks and ETF’s

2. You select a broker with low costs 3. You only purchase stocks or ETF’s that you understand. When the price hits or drops below your purchase price, you always SELL. |

|

Review the risks |

You know that you take risks by driving a car. Anything can happen. You always lose money as a car depreciates in value over time, you also pay maintenance and insurance costs | You know that you take risks by investing in the stock market. You only lose money when you sell below your purchase price. You can only gain money if you follow strict investment rules. |

Did you read every line of the above table? Maybe you think…well this is not an analogy. Really why? Do you think that growing your money is NOT a necessity? So you want to invest time in learning how to drive a car but you don’t want to learn how to grow your money. Second excuse is investing in the stock market is risky business. Really..do you think it is more risky than driving a car. I believe that there are more risks involved when driving a car than investing in the stock market. Are you afraid to lose all your money?

How do you manage risks in the stock market ? Here are my 3 rules to manage risk in the stock market

- Risk avoidance : you only invest in what you understand. Know what the company does or what the ETF is composed of. Know how much dividend you will receive on your investment.

- Risk reduction : you only invest 10% of your portfolio in one investment. You diversify your investments so you can limit your risks when you pick one bad investment.

- Risk acceptance : When you invest in the stock market, you know that there is risk. The same risk as when you drive a car. There are more risks driving a car than investing in the stock market. When you make a wrong investment, you sell at cost price or at a Maximum loss of 5% of your investment. The biggest mistake investors make is assuming that the stock price will go up over time…well, it may never go up! So always cut loose your bad investments. You can’t win them all. It is part of risk acceptance. When you drive a car, you also accept that you can have a flat tire, right? You also accept that somebody will crash your car, right? Hopefully without any physical injury. Well, with stocks, you can lose 10, 20 , 60 or 90% of your investment. Maybe everything… It has happened to me in the past. Now I always sell when the stock drops 5% below my purchase price (if possible). Re-investing that money quickly recuperates that loss…you will see.

3. Our final conclusion

The survey showed that the Belgians have no appetite for risk and they save 186 Euro on average. They put it on a savingsaccount which give them NO return on money saved. For every 10.ooo euro a Belgian places on a savings account, he loses 200 euro. I don’t understand this.

The Belgians have no appetite for risks. But do they understand the risks of the stock market? Do they have any knowledge of risk management? If they understand the risks of driving a car, do they understand the risks of investing in the stock market? I wonder…

When I started with my Dividend Investment strategy, I started with 40k. It was all I had left after a divorce. Did I risk losing all my money by investing in the stock market? No. Never… because during 2014 I first invested in my financial education and how to manage the risks. In 2015 I was able to generate 3383$ out of this portfolio. That result equals like 280$ per month. That is more than the 185 Euro per month that a Belgian saves per month…imagine that…

I end with the quote of an intelligent investor who states it correctly! If you want to grow your money as badly as you want to drive a car, you will invest in your financial education and learn how to manage risks ! Change your attitude… learn how to invest like you learn to drive!

Good luck with your personal finance strategy ! Keep on following us on Twitter and Facebook where we share more blog posts and other articles.

9 Response Comments

It is contrary to see people save a lot of money in order not to loose on the stock market. Current interest on the best savings account can not keep up with inflation. So, they loose.

To me, not investing is taking a risk. The risk of not having enough money once retired.

I can’t agree more !!

I must say it was hard to find your website in google. You write awesome posts but you should rank your blog higher in search engines.

If you don’t know 2017 seo techniues search on youtube:

how to rank a website Marcel’s way

Thanks for the feedback ! I know I still have some work to do to rank higher in Google.

I look forward to your future feedback and comments.

Hello Patrick, I am Belgian and could not agree more with your conclusion. I even have friends who are very good at saving but that are so reluctant to start investing in the stock market or any other better uses for their hard earned cash to flourish! It can be very rewarding to invest in stocks and get involved more in a company you like or where one sees potential. It can also be rewarding to invest in real estate, you get to be part-time entrepreneur and another income stream. Let’s continue spreading the good word! 🙂

Thanks Jonathan !! I know real estate can be rewarding but the return in Belgiun is 3%. Little higher than inflation. Not rewarding enough for me (at this moment) I continuously look for creating other passive income streams. Great blog

Yes returns are low for RE in Belgium I agree. Thanks 🙂