April 2019 . Easter vacation time for the kids is ongoing. A moment where I take a big envelope and put memories of the past year events, pictures, drawings of the kids and send it to our foster child in Nepal. I also add a tourist guide of cities where I have been this year. Instead of trashing it with the paper trash, we can give a child in Nepal a perspective on a world city like Amsterdam and Easton in the USA. She can at the same time practice her English.

Now it’s also time to reflect on how we grow the money for our foster child. Our last update dates from April 2018…did our portfolio grow in the meantime ? But let’s repeat why we are doing this.

Why investing money for a foster child ?

As outlined in our Portfolio of our foster child, during the past twenty years I have travelled the world and seen more than 20 countries. One key insight that did touch my heart, was the poverty of kids in certain countries. In order to have a better life, it is SO important to have the right education to achieve a better lifestyle. I have seen kids living on the streets, kids who had been burnt in their faces to continue their lives as beggars, kids who were starving, etc…I have seen kids in life conditions that I will never forget in my life.

For that reason I have decided to support a child within Nepal through the organisation Cunina. Cunina shares the same dream as I do have. They believe that every child is unique, is talented and deserves a chance to develop these talents. That’s why I support Anisha, a girl in Nepal.

If you want to learn more about Cunina’s fantastic work, go to their website www.cunina.org or download the English brochure of Cunina.

My commitment to Anisha is to pay her education (30 Euro per month) until she graduates from university. Then my relationship with Cunina will end. However that does not mean my relationship with Anisha needs to end…

We do follow the situation in her country and came across the following interesting publication of Damir Cosic from the World Bank Group.

Climbing Higher: Toward a Middle-Income Nepal

Last year we wrote about the fact that the minimum monthly tea-work-related salary will increase to NPR7,075 (about US$67) and the daily wage to NPR253 (about US$2.40). This year we take a look at Nepal’s situation as a country. The publication of the World Bank Group doesn’t project a great outlook for economic development of the country.

Nepal’s recent history of development is marred by a paradox.Many countries in the world have experienced rapid growth but modest poverty reduction, as income has increasingly concentrated in the hands of the wealthy. Nepal, however, has the opposite problem—modest growth but brisk poverty reduction. The country has halved the poverty rate in just seven years and witnessed an equally significant decline in income inequality. Yet, Nepal remains one of the poorest and slowest-growing economies in Asia, with its per capita income rapidly falling behind its regional peers and unable to achieve its long-standing ambition to graduate from low-income status.

Challenging development constraints have been further compounded by unsupportive policy choices. The economic history of Nepal over the past 45 years provides important lessons. The resulting current state of Nepal’s economy not only reflects the challenging constraints to development, but also policy choices that have resulted in weak performance of the large agricultural sector, low public investment and capital accumulation, and low productivity growth. During the past 45 years (1970–2014), Nepal grew at an average annual rate of 4 percent, while the growth rate of per capita income was the lowest in South Asia, averaging just 2 percent during this period.

Given this backdrop, it is not surprising that outward migration has grown in importance, especially in the post conflict period. In FY1996, approximately one in four Nepali households received some form of remittances. This became one in three by FY2004 and more than one in two by FY2011. Not only did more households start receiving remittances, but the amount of remittances received also increased over the years. The first half of the 2000s saw a drastic increase in remittances, from 2 percent of gross domestic product (GDP) in FY2000 to 15 percent in FY2005, 22 percent in 2010, and as much as 30 percent in FY2016, making Nepal the highest recipient in the world among countries with a population of over 1 million and measured as a share of the economy. Given the phenomenal rise in remittances, they are likely the primary engine behind the improvements in living standards witnessed in Nepal, both directly (households receiving remittances) and indirectly (increased labor income of those that remained).

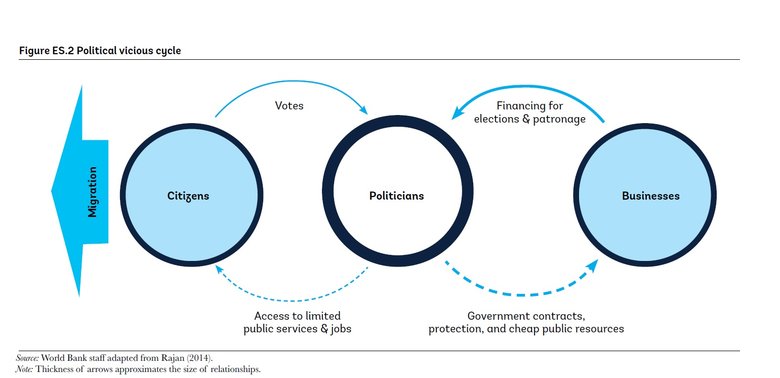

Perhaps the most detrimental aspect of large-scale migration is that it relieves the pressure on policy makers to be more accountable and to deliver results. Large-scale migration solves several problems for Nepal. It alleviates unemployment; enables greater consumption; and leads to higher tax collection, given the high dependency of taxation on imports (currently generating half of all revenues). At the same time, it lessens the pressure on the political class to break with the long history of trading favors for patronage. Frequent change of governments has become a long-established norm; the country has had 22 governing coalitions in the last 26 years. This political instability has hampered the country’s development and disillusioned its citizens, contributing to further migration (Figure ES.2)

Without comprehensive reforms to address its long-standing challenges, Nepal will probably not become a lower-middle-income country before 2030… that doesn’t sound promising.

Our Objective

Portfolio Update

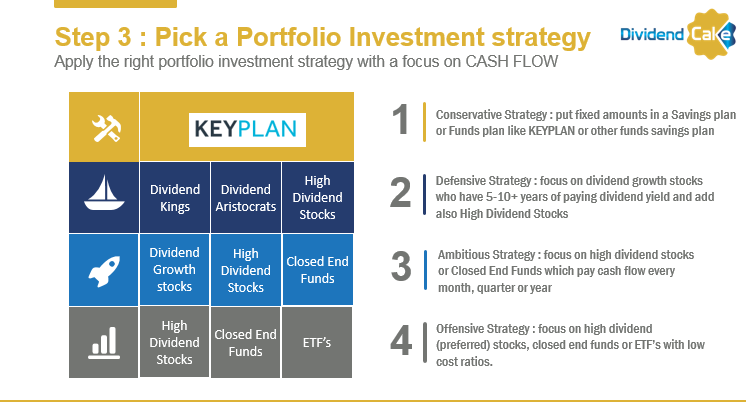

Today I put monthly 25 EURO in a KEYPLAN and you can read below what has been the return so far. KEYPLAN is our FIRST conservative investment strategy in our Portfolio Investment strategy.

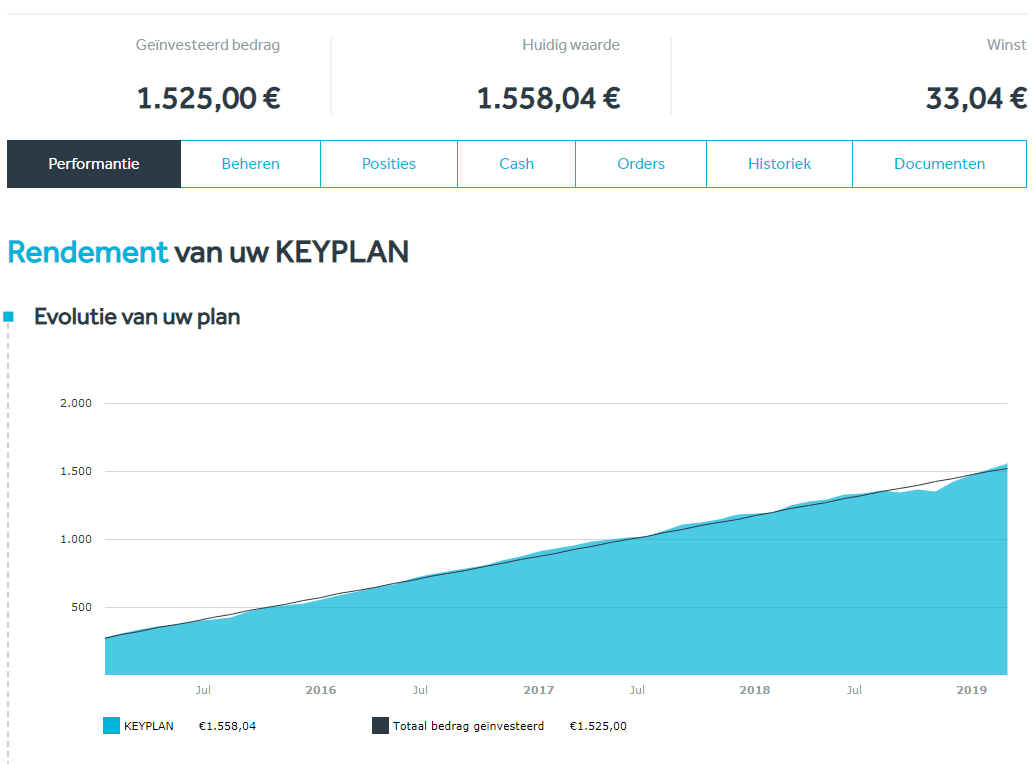

Last year the money we invested was 1225 Euro and it had generated 11,14 Euro extra money. The diversification of the money is spread amongst 11 different funds. Today we have 1525 Euro invested and we have 33 Euro profit.

Please be aware that this strategy aims two factors: TIME and BUY ON FIXED TIMES. The funds do not generate any dividend income and the strategy of compounded interest does not apply here. The only extra income is my monthly 25 euro each month that purchases new participations in the funds. It is important to remain invested for at least 5 years, otherwise this strategy cannot be successful.

Below you can find the performance chart.

Since 2015 achieving only 2% on the invested amount is embarrassing. That is LOWER than inflation and so I am losing money here… I am considering to stop this strategy going forward. I think the biggest winners are the fund managers here. So we will reconsider our strategy and see how we can achieve a higher % return for a small account. Okay, I didn’t lose money so far but if the stock market turn, this portfolio will drop in value. Take a look at the graph and see the dip in December.

Final Note

I have a strong belief that EACH ONE OF YOU can change one other person’s life in the world. I see many people spending money on materialistic things …but does that make them any happier? Each person decides for himself their purpose in life and their objectives. One of my perspectives is that if you can change someone’s life towards a better life, this world would definitely be a better place.

That purpose in life means YOUR LIFE DID HAVE A SOCIAL IMPACT. We have now achieved 31,2% of our long term portfolio objective.

This is the end of our blogpost.

If you haven’t subscribed to our newsletter yet, please do so. Life can be busy sometimes and people lose track of following a personal finance and travel blog. Subscribe and you will get one email per month highlighting what you missed…

Thanks for following us on Twitter and Facebook and reading this blog post. We end with a quote as always.

No Comment

You can post first response comment.