Hi everyone,

the first 2 weeks of May are already behind us. It’s amazing how time flies…here’s our 4th Dividend Income report for my mom’s portfolio

Did my mom travel in April 2017 ? Yes, she did…She went for a weekend with friends to Blankenberge at the coast of Belgium. But during that weekend, someone of the group passed away over night. My condolences to his family. And this sad occurence made my mom realize how fragile life can be…

Why your retirement planning is IMPORTANT

In my blog post of last week Wednesday, I reviewed the Belgian retirement system and how the government institutions will consume all net worth. A political party CD&V wants to oblige kids to pay for the financial costs of their parents. You can read my opinion about this proposal and why your retirement planning is important in this blogpost.

How you can lose all your net worth and make also your kids poorer…

My mom is also concerned about her finances going forward. As described in Portfolio of my Mom strategy, my mother will be 800$ short if she needs to go to a retirement home. Her pension will NOT be sufficient to pay a pension home. The cost of a retirement home is at least 2000 Euro per month. My mom does not know the return of her capital, neither has any financial knowledge. Therefor it is CRITICAL to activate her sleeping capital AS SOON AS POSSIBLE. Her savingsaccounts do not generate any passive income.

If you are in your 20’s or 30’s (or even older), it is important that you read also the following older blogpost I wrote last year Get rich at your retirement – Learn how?

This blogpost clearly describes the strategy on building out a portfolio which will support your lifestyle without jeopardizing your net worth going forward. You can no longer rely on the government to build a pension which will cover your standard living expenses. It is sad but it is a fact which we will need to adapt to. In some countries I see people emigrate to another country where the standard living expenses are lower and health care is still qualitative. For example, couples in pension from US move to Costa Rica or Panama. People from Germany move to Hungary..

If you have read our Financial Strategy, you know that layer 2 in our financial pyramid is a Pension Saving plan. Read all our blog posts within the category Retirement if you want to read more.

My mom has also adapted IT technology in her life. While she was using a NOKIA mobile for many years, one day she was forced to change. Then my mom purchased an iPad mini and iPhone (on recommendation of her grand kids) to connect with friends and she is also using it now to follow up her portfolio. Her grandkids are also pleased with such a modern grandma. That’s why I picked this picture for this blog post.

Now you can read our Dividend Income April 2017 Report Out for my mom’s portfolio.

Dividends received in April 2017

During the month of April 2017, we received 410,18$ dividend income. A new monthly RECORD !! You can imagine that we are very HAPPY about that monthly result ! This is 50% of our ultimate objective.

This dividend income was composed of 151,80$ monthly payments and 258,38 Dollar from high yield quarterly paying ETF’s . Our 5k investment on 29th March has resulted in a nice upwards result, don’t you think? It is a 21% growth compared to January 2017.

![]()

Portfolio management

During the month of April, we also executed some changes in our Mom’s portfolio. We sold our position in the European bank as this position would be doing NOTHING in our portfolio during the coming year. We can not expect any new dividends for another year. That’s why I don’t like European stocks and ETF’s. Money needs to work for me. I don’t want to wait for possible capital gains…

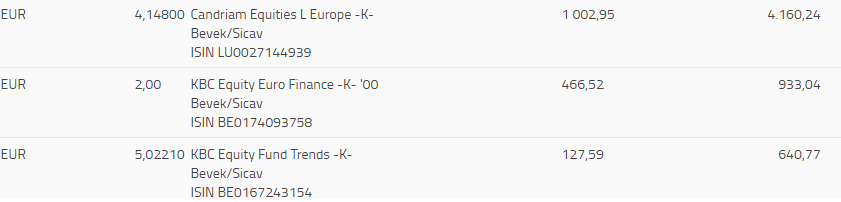

We reviewed the performance of all remaining funds in my mom’s portfolio at the bank and continued to clean up the high cost mutual funds. We sold again three funds. See screenshot. One fund had a performance of 2,64% and another one 3,85% since years . They do not even cover the cost of the mutual fund. The cost of the investment is also too low to generate capital gains compared to the cost of the mutual fund. I can not understand why banks keep on recommending these investments to people. When I enter a bank office, I always see on a white board FUND OF THE MONTH…it’s similar to walking in a gardening shop where they sell the FLOWERS OF THE MONTH. Did you notice that too?

When I asked the bank to sell those three mutual funds, it took more than 3 days to execute. Can you imagine? When I sold the shares of this European bank, it was done within 5 minutes…Another reason why you need to manage your investments yourself !

So we transferred this amount to my mom’s investment account which increases our cash position. Our portfolio has now a market value of 23700 Euro which includes a 1000 Euro capital gain. The 1000 dollar cash received from my investment portfolio is not reflected in the return on investment of our broker. So we are still invested below 25k. Our cash position has increased due to the sale of all costly and non-performing mutual funds.

There are three mutual funds remaining in the portfolio of the banks. These three funds have a %return above 20% since the date of investment. However the real % return per year may be a lot lower due to the fact that mutual fund costs are not included in the % net return calculation. So I consider it misleading information…

It will depend on the direction of the European stock markets on what I will do with these mutual funds.

Dividend Income Growth

Now my mom’s dividend income has accumulated to 906,74$ and 111,62 Euro. If we add this up, we have a total of 1026,03$. We already exceeded the dividend income of previous years last month but now we can really grow our cash flow tree.

The total yearly dividend is 86% of our YEARLY OBJECTIVE of 1200$. There’s no doubt we will beat our yearly objective.

![]()

Going forward

We are now in May 2017. We have build up our cash position by cleaning up the mutual funds and our FIRST 1.000 DOLLAR dividend income is also on our bank account.

We will definitely beat our yearly goal of 1200$ so now it’s time to set another SMART goal. I believe also (without doing the math) that our monthly payers are now paying above the yearly objective of 100$. So with our current cash position…can we grow our monthly cash flow payments ? Are there still undervalued stocks or ETFs to be found in the stock market ? Some analysts say the stock market is highly overvalued…I remain cautious as always and look out for new opportunities. Opportunities can always be found in the stock market….you just need to know where to search…isn’t it?

So our NEW MONTHLY DIVIDEND INCOME goal for 2017 will be 200$. Can we grow the cash flow from my mom’s portfolio to 200$ per month? I did not do the math what our new yearly objective would result into. I don’t consider it important. We will target as HIGH as POSSIBLE.

Remember that the ultimate objective for my mom’s portfolio is 800$ per month to support her retirement plan. We are still far away from this but in April 2017 we reached 50% of that objective. So that motivates me ! I can NOT allow the sharks of government institutions to eat my mom’s net worth away when she needs a pension home one day. I hope she doesn’t need one in the next 10 years so I can continue to build her cash flow trees.

How are you doing with managing your finances? Do you put your money at work and grow your cash flow tree? We hope so ! We end with a final quote.

This quote nicely reflects the four portfolios we manage today. 4 portfolios, 4 strategies, 4 objectives. We are planting now and harvest month after month…

4 Response Comments

Can you give examples of High Yield Quarterly Dividend paying ETF’s you use. I’m interested in those. Also interested in which broker you use and or how you minimalize broker fee’s.

Hi Pieter, I have send you an email with all the responses. Thanks for stopping by and keep on following us !

Another great month, well done to you.

It is an interesting story to follow…!