Two weeks ago I spend another week in Pennsylvania, USA. One advantage of those business trips is the free Wallstreet Journal every morning. In one of those morning editions, I did find a Special Report of Barron’s.

Sarah Max wrote about “The 4 Steps to teach your kids about MONEY !”

Gottlieb’s mother explained the value of the dollar, even pointing out that, because of taxes, she actually had to earn more than $10 to keep that amount. “My mom and I had plans for the two of us to go to a restaurant for dinner that evening, and I was really looking forward to it,” she says. “She canceled our dinner and instead made me a peanut butter and jelly sandwich.”

It’s a lesson that has stuck with Gottlieb. Kids can begin to conceptualize money around the time they’re in preschool. Though money is a less taboo topic now than it once was, teaching key concepts about it might be harder today, in a world of what Gottlieb calls “invisible money.” Even pulling out a credit or debit card seems quaint when consumers can flash their phones to pay at the checkout or buy something in their social-media feed with one click.

While the economy is, by some measures, robust, many young adults say that money problems cause constant stress; consumer debt in the USA is increasing faster than household income, and an astounding 36% of US millennials—people now 23 to 38 years old—surveyed by Schwab have no savings for emergencies.

If ever there was a time for parents to talk with their kids about money and instill good financial habits, it’s now. “As they say, small kids, small problems; big kids, big problems,” says Gottlieb, who works with multigenerational clients. Read this sentence again. This counts for all countries !

There’s no single playbook for what, when, and how to teach kids about money—your circumstances and the child’s personality are part of the equation—but one tactic is universal: “Parents should use milestones in their kids’ lives to sit down and have a conversation,” advises Tim Ranzetta, founder of Next Gen Personal Finance, a nonprofit that provides educators with free resources to teach personal finance. When your tween lands a babysitting gig, talk about saving. If your 16-year-old is on the verge of getting a driver’s license, discuss insurance. As college decisions come into focus, make tuition, student debt, and career plans front and center.

Here’s how parents (and grandparents) can set up kids for good money habits:

Early Childhood: Teaching by Example

Just as children develop language skills by hearing words, they develop ideas about money by listening to, and watching, their parents. “They are little sponges taking in how you make decisions related to money,” says Scott Rick, an associate professor of marketing at the University of Michigan and father of three young kids.

In a recent study, Rick and fellow researchers found that children as young as 5 had distinct emotional responses to spending and saving money, suggesting that people are prewired to be spendthrifts or savers. This isn’t to say spendthrifts are doomed to making bad decisions or that savers will be misers. “Parents can help kids recognize the emotions around money and help them adjust their behaviors,” Rick says.

In a recent study, Rick and fellow researchers found that children as young as 5 had distinct emotional responses to spending and saving money, suggesting that people are prewired to be spendthrifts or savers. This isn’t to say spendthrifts are doomed to making bad decisions or that savers will be misers. “Parents can help kids recognize the emotions around money and help them adjust their behaviors,” Rick says.

The best place to start is giving youngsters a window on spending and saving. Routine outings to the grocery store, for example, present a great opportunity to talk about the basics: Money is a limited resource; things cost money, and every spending decision comes with a trade-off.

Personally I emphasized many times to the kids at young age that money is a LIMITED resource. Saying NO to a spending decision helps to make a difference between a NEED and a WANT.

Tweens and Early Teens: Practice Makes Perfect

Young children start to understand the difference between needs and wants, but this takes on real weight when they enter middle school and what they want costs more than a candy bar. Cellphones, soccer fees, and expensive sneakers make money lessons very tangible.

Here’s where the training wheels should come off. Regardless of how great your means are, don’t give your kids carte blanche for routine expenses. Instead, devise a budget and come up with an allowance. Personally I started to give the two boys 30 euro every 2 months. One likes to spend it and the other saves it all…

The jury is still out on whether kids should have to work for their allowance. Some say that the only real way to appreciate the value of a dollar is to earn it; others argue that it’s more important to teach youngsters to be accountable for their spending. “But the bigger point is that kids need to practice managing their own money, and that often means giving them an allowance,” says Ranzetta.

Experts emphatically agree on two points: First, the allowance should be paid monthly or even quarterly, so that the recipient must make it last. Second, parents should outline clear parameters about what’s covered by the money—and not cave in if it’s spent quickly and the child pleads for more.

Teens to Pre-College: Holding Them Accountable

This is when life milestones—and related money matters—come in rapid succession. For many teenagers, it starts with getting a driver’s licence, use of a car, or possibly their own vehicle. “This is an ideal time to introduce the concept of insurance,” Ranzetta says. Premiums and deductibles don’t make for titillating conversation, but if getting the car keys is predicated on understanding them, kids will listen.

Parents should help their teens update their budget—or create one if they haven’t done so already—and encourage them to use their new mobility to make extra money. When they start to earn a real paycheck, drive home the value of saving and introduce basic concepts of investing, including the value of diversification and tax-advantaged accounts. Personally I also intend to teach the three kids the value of investing your money wisely.

College and Early Career: Preparing to Launch

Decisions made during this stretch can have lasting financial implications, whether related to student debt, career prospects, parents’ financial goals, or all of the above. “Parents should start these conversations early, before they and their kids make decisions that will follow them around for quite some time,” says AICPA’s Westley.

College money conversations should include costs, budgeting, and the desired outcome. Assuming your child has managed money in high school, the financial transition might not be too jarring in the freshman and sophomore years, thanks to student housing and campus meal plans. Upperclassmen often move off campus—or have internships that require living on their own—and that opens doors for conversations about rent and utilities, budgeting for food, and earning money.

In any case, “once you’re 18 years old, you can start making some serious financial decisions, and bad decisions can start mounting up pretty quickly,” Westley warns. While student loans loom large, credit-card debt can be the bigger concern. In a recent survey of 30,000 college students at 440 institutions, 36% said they already owe more than $1,000 on their credit cards. In Europe people don’t have so much debt as in the USA and I will personally teach the kids to avoid debt with ALL means and teach them the value of financial independence.

Here’s the thing: Regardless of whether your child is 3 years old and buying something with her own money for the first time, or 23 and paying her own rent, there’s tremendous value in financial independence. “That moment when a young person can feel like they have agency, where they actually can drive these decisions,” says Ranzetta. “It’s extremely energizing and empowering.”

And it’s something that parents should remember when they’re finding it hard to teach their kids financial literacy.

Passive Income Update 2019

During the past months from September until December, our dividend paying stocks and ETF has been paying us dividend. I also wrote two options

- SIL Put 18 October for 116.27$ at 28 strike price

- NUGT Put 22 November for 101.27$ at 25,5 strike strike

That’s how I cashed another 227$ in this portfolio.

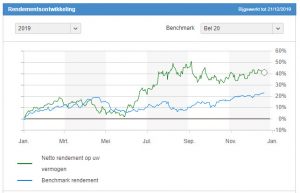

Portfolio 2019 Performance

Our kids portfolio has performed very well in the year 2019. Below you can see our yearly performance against the BEL20 index. In total we cashed more than 1500$ which is NOT included in below performance chart.

Going forward

So we banked another 200$ thanks to 2 options we wrote. That brought our YTD total above 1500$. Our cash position is shown in the table at the side. The value of our portfolio is above 14K.

So we banked another 200$ thanks to 2 options we wrote. That brought our YTD total above 1500$. Our cash position is shown in the table at the side. The value of our portfolio is above 14K.

This is the end of our blogpost. Did you realize more than 1000$ for your kids or do you keep on saving money in a savings account ? No ? Then you should start investing in your own knowledge. Putting your money on a savings account is not a strategy to grow your kids money.

If you haven’t subscribed to our newsletter yet, please do so. Life can be busy sometimes and people lose track of following a personal finance and travel blog. Subscribe and you will get one email per month highlighting what you missed…

Thanks for following us on Twitter and Facebook and reading this blog post. We end with a quote as always.

Source : Barron’s

No Comment

You can post first response comment.