Three months until the year end. Coming months I have plugged in several investors events in my calendar. Also some abroad. One of the events that interested me, was the presentation of Sam Hollanders. I did meet Sam personally during past VFB investors events and I was interested in his way of looking at companies and his underlying strategy to invest.

Read below our summary and key learnings.

Who is Sam Hollanders ?

Mr. Hollanders is a stock investments author, specialized since 2004 in value investing. He is the author and genius behind the scenes of several websites. I list them out :

Mr. Hollanders is a stock investments author, specialized since 2004 in value investing. He is the author and genius behind the scenes of several websites. I list them out :

- Beursloper : www.beursloper.com

- Smart Capital : www.smartcapital.be

- Brokertarieven : www.brokertarieven.nl

Whether you want to compare broker costs, learn how to invest with a course, or subscribe to a stocks tips newsletter, you can find it on one of the above websites. Sam uses the broker Tradersonly ![]() for his portfolio. If you follow our blog, you know we recently switched two of our portfolios to this broker for lower costs. Costs do bite away your gains, so you must limit your investments costs as much as possible.

for his portfolio. If you follow our blog, you know we recently switched two of our portfolios to this broker for lower costs. Costs do bite away your gains, so you must limit your investments costs as much as possible.

Let’s go to the summary of Sam’s presentation.

Summary of the Presentation “Quant, Growth or Value Investing ?”

The title sounds like taken from the bible. Goal of the presentation is to give you a long term perspective and how to anticipate from a short term perspective. The agenda of the presentation is :

- Value investing why ?

- Each company can be good or bad investment…

- Why making difference between value, growth and/or cheap

- What is Quant investing and why you encounter this a lot…

- For the students : How to become rich while you sleep

What is Value investing ? You can get inspired by Warren Buffett. Sam recommends to read the book of Charlie Munger and how he uses his investment strategy. Berkshire Hathaway’s visionary vice chairman and Warren Buffett’s indispensable financial partner, has outperformed market indexes again and again, and he believes any investor can do the same. If you apply value investing, growth is part of the value calculation.

What is Value investing ? You can get inspired by Warren Buffett. Sam recommends to read the book of Charlie Munger and how he uses his investment strategy. Berkshire Hathaway’s visionary vice chairman and Warren Buffett’s indispensable financial partner, has outperformed market indexes again and again, and he believes any investor can do the same. If you apply value investing, growth is part of the value calculation.

When is an investment a good or bad investment ? When do you buy a company ? Is the price value cheap or expensive ? You only want to have 1 variable. So you can fill in the growth and put the price of the stock in the valuation. 3 years -> 50% growth -> price x 8.

Sam gives an example : Lotus Bakeries

P/E is 15. At which growth is the current value then a fair value for a period of 3 years? 8,3% growth by the market is priced in today. Is this achievable? The growth for Lotus past years was around 3%.

Calculating of the value of a company is a bit “guess-timation”. There is no magic bullet. Sam shows the formula for value investing. The variable is the estimated return. For example 15%.

There are a few companies that “seem” to be there forever. Kodak, Compaq, Polaroid, Van de Velde? Maybe Agfa Gevaert is also a candidate as the pension burden is huge. The products are great but according to Sam we still have to wait 4 – 5 years before the company can generate value. He also shows a slide with bad companies.

Bpost – Nyrstar – Option. Bpost is a bad company because the Belgian government is shareholder. SmartPhoto is another story where they made a turnaround. The key question is what do I pay for a company? What is the share price? Oil shore drilling companies are an example of companies that can be bought cheap.

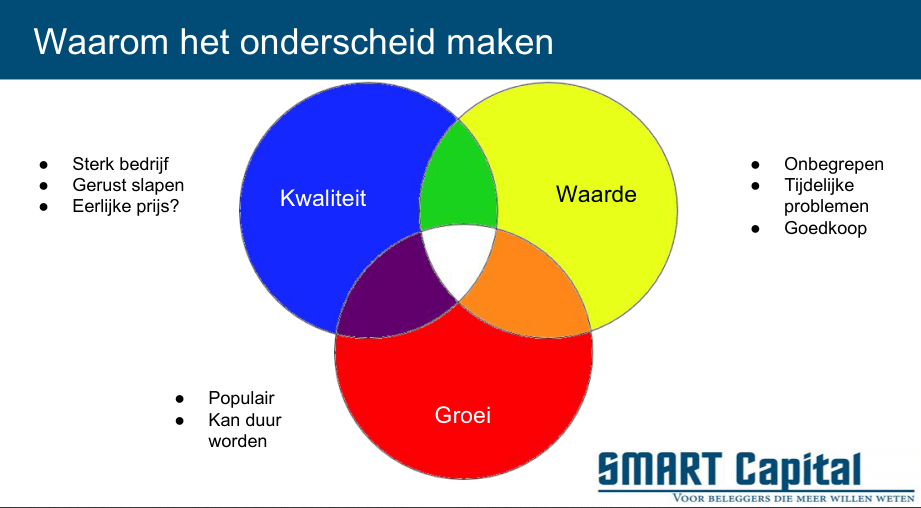

Why should you as an investor make a difference between quality, growth and value ? You want to chose the white color. These are the perils who are hard to find. You need to judge based on Quality, Value and Growth.

Let’s review the 3 criteria. Criteria 1 Value : here you find companies that are not understood, have temporary problems, are cheap, are maybe in a sector that is currently not wanted, …

Cheap stocks are easy to find. In Yahoo Finance you can search on EV/EBIT and P/Book value. Operational Profit and Net Cash Flow are the most important to review. Examples at Euronext with low P/B are Qrf CityRetail and Euronav.

QrfCity Retail is valued by REIT experts. Qrf is valued at a price of 22 Euro. The current price is 16 euro. That is a discount of 30%. This and next year will be a bad year for the real estate investment company. The management team is strong and knowledgeable in the sector.

Euronav operates in a cyclical market. One day the oil sector will rebound or an alternative can be found for transport. A bad example is D’Ieteren.

Criteria 2 : Quality

Here you find companies with a competitive advantage. Companies with strong brands or global leverage. Also companies who have limited access to certain markets is a competitive advantage.

How is the management team ? Honest, Intelligent and integrity are key values for great management of a company. Picanol is an example of management turning the company around. Quality companies are also companies who pay a dividend for many years. Dividend investing is more popular in Netherlands. In Belgium the government bites a big portion out of your dividend payout. Constantly paying a (growth) dividend is definitely a factor of quality.

How do you value Quality? Here you have the Scuttlebutt method of Fisher :

- Potential of the products

- Long term growth

- Plans to grow

- Research and development

- Sales department

- …

In a growth company, the CEO is the best sales person of his company! That is a networker who knows how to deal with people. In yearly earnings reports Sam searches for the growth plans. Not all growth plans are executed tough, he concludes.

An example of Quality : SIPEF

Nobody wants palm oil. Bad reputation due to forest destruction. 24% destruction of forest is to farm animals. Only 5,4% is for palm oil plantations. SIPEF is 100% RSPO certified. 68% of palm oil is used in food (chocolate, ..), 27% in beauty and household products.

A discussion around the studies in palm oil between the public and Sam sparks off…lol. It’s all about the palm oil perception, the RSPO certification, the production % going forward,…

Criteria 3 : Growth

Growth companies are constantly in the news. Bad news on fast growing companies travels fast. What is risk for investors? When a stock price of a company has High price and High Risk, then stay away.

Cash flow, Net profit and Operational Profit are three most variables to evaluate. The orange piece : Cash burners are examples.

Sam shifts the presentation to diversification in a portfolio.

How much money is in your portfolio? You need to evaluate your % capital allocation according to Quality, Growth and Value. That’s how you diversify. Diworsification is a terminology that can apply for quality stocks. The key is to allocate the stocks in the white box. Extremely difficult. The margin of safety is KEY for value investing.

How much diversification? When you have 32 stocks, you already have 96% lower risk in your portfolio. You need 500 stocks to have a 99% risk avoidance profile. “Finding the right stock is the same as a lady that finds the perfect shoes in a shopping mall.”, Sam quotes.

So what is Quant investing ? Quant investing is investing based on data. The magic formula of Joel Greenblatt is all about a simple idea : Cheap, Quality and best Value ratio. This resulted in a profit return ratio of 30% yearly between 1988 and 2004. Not everybody is using the formula as there were 6 years the market was not beaten.

Several other studies appeared as a result. Piotroski, Beinish ,… Basu, Fama & French are different methods. Richard Tortoriello wrote a book “ Dual Momentum Investing” about quantitative strategies for achieving alpha.

What if we combine the three factors ? Quality, Value and Momentum. Back testing was performed in Europe (June 2001 and August 2014) and US between 2001 – 2012.

30% of the times the formula doesn’t work and then the human factor kicks in…emotions. We are not programmed to follow a system like a slave. What is Smart Capital using ?

Uncle Stock Screener, Vector Vest, Quant Investing, Value Signals are some of the tools used by Smart Capital to identify the right stocks.

Sam ends with some key messages for the students in the room. When a newspaper publishes a compound interest table full of errors, you have to say to yourself “Fake news!”

You can become rich while you sleep in one simple way. Invest in holdings….owned by rich families. Ackermans & Van Haaren, Sofina, HAL Investments, Brederode and Investor AB (Swedish) are some good examples.

Mutual funds at the banks have 1,5 or more % costs. Holdings only have 0,14% cost factor. Holdings resulted in a 7,8% in the last 18 years. So if you invest each year 1200 Euro that gives you after 40 years..€338.420. But if you invest the first 5 years 2400 Euro per year, you achieve €213.973 and you only invested 12.000 Euro. So you invested the first 5 years and achieve €213.973.

If you want the presentation and an excel file with the magic formula, go to www.smartcapital.be/vfbtrefpunt

Final Note

What did we learn ? The first important lesson was how Sam makes the split between value, growth and quality. I think this is a fundamental thinking that every investor should apply. The second key learning was the set of tools used to identify value companies and how to screen for stocks. Personally I don’t use such a set of tools as I am a different type of investor. If you follow the blog, then you know I focus on different strategies for the 4 different portfolios. The main strategies are dividend and options investing.

I hope the key messages for the students were understood and taken seriously. Investing a portion of your portfolio in holdings is a solid strategy. This concludes my blogpost which I wrote on the plane…high in the sky ! You can find the proof at the side…Internet in a plane. Technology never stops !

Don’t hesitate to leave your comments and feedback. Let us know what you think.

Good luck with your personal finance strategy! Thanks for following us on Twitter and Facebook and reading this blog post. As always we end with a quote. This time with a quote that Sam used during his presentation.

No Comment

You can post first response comment.