In the week of 24 April, a CD&V parlement member Nahima Lanjri wants to put forward a law to oblige kids to pay the invoices and costs of the pension homes where their parents live during their pension.

How does the Belgian Retirement System work ?

When you retire you receive a pension from Belgian government as you paid HIGH taxes all your life. When people need to live in a pension care home, there’s an invoice to be paid. The costs are paid by the Belgian instituton (Riziv) but the hotelfees are invoiced against a daily fee to the pensioned man or lady living there. In Flanders this invoice is on average 1.500 Euro per month. In reality you can say it is more around 2.000 Euro.

For all payments the system looks first at the pension of the person. If the pension is not sufficient to pay the bill and you don’t have any savings, the person can get help from Flanders’ OCMW – the Public Centre for Social Welfare.

What does this Public Centre for Social Welfare do? They review first all your net worth such as savings, your house and your portfolio. If the person has sufficient net worth and capital, the person needs to consume all his savings, rent or sell his house,…to pay all the bills. They will not pay any bill. This Public Centre for Social Welfare requests first to be completely BROKE or in another word POOR AND NO MONEY LEFT before intervening with any financial aid. This OCMW institution can even put a loan on your house so when it is sold they recuperate all their costs…

What does this Public Centre for Social Welfare do? They review first all your net worth such as savings, your house and your portfolio. If the person has sufficient net worth and capital, the person needs to consume all his savings, rent or sell his house,…to pay all the bills. They will not pay any bill. This Public Centre for Social Welfare requests first to be completely BROKE or in another word POOR AND NO MONEY LEFT before intervening with any financial aid. This OCMW institution can even put a loan on your house so when it is sold they recuperate all their costs…

What happens if YOU can not pay …

When all your savings are consumed, your house is sold or a loan is put on your house to cover the bills, this OCMW can still claim the remaining costs towards your kids, who are legally obliged to pay the costs of their parents and parents-in-law. When there are multiple kids, the costs can be divided equally.

If the salary of your child is not above 18.418,6 euro (increased with 2.578,60 euro for every person at his cost of living), the OCMW will not request to pay. The higher the salary of your kids, the higher contribution requested to your kids…

If the yearly salary of your child is more than 60.000 Euro, the contribution can be 995 Euro per month. Crazy, isn’t it?

Why does this political party CD&V want to FORCE kids to pay?

Today it seems that dependent of the local city or village you live, you are either obliged to pay or not. This political party wants to OBLIGE KIDS in all circumstances to pay. While in 2009 the same political party didn’t want kids to pay after paying years of taxes, now they flipflop differently and want to force kids to pay in all circumstances…

On television, there was an example of a couple where the son explained that his two parents required to live in a pension home. Total monthly bill : 5.000 Euro per month. The total sum of the two pensions of his parents are 2.400 Euro. While the OCMW institution was consuming the net worth (all savings of his parents), he as single child was required to pay 400 EURO per month on top. This was putting a major financial burdain on this family with little kids and also causing family discussions within his marriage. His family was not able to pay family vacations…

Our opinion

Conclusion 1 : Your pension will NOT be sufficient to support your standard living expenses in a pension home

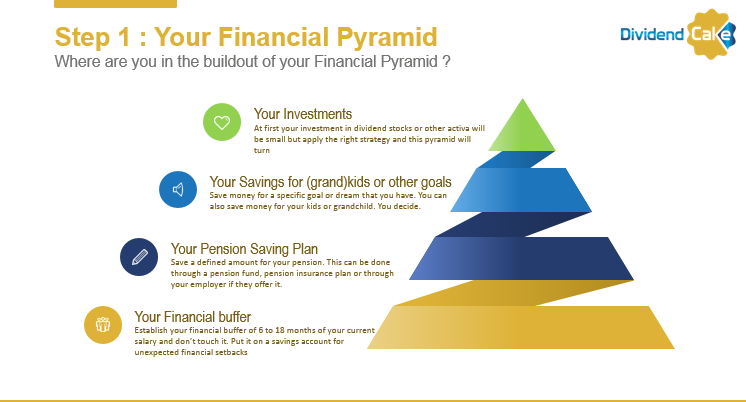

When you need care in a pension home, your pension will not be sufficient to cover all the costs. You need at least 2.000 Euro per month. The earlier you start with a Pension saving plan (even multiple ones) the better for your retirement. If you don’t have anything in place, you should start TODAY. A pension fund plan is also for 30% tax deductible.

See our Financial Pyramid with Layer 2 your Pension Saving plan.

Conclusion 2 : If your investments do NOT generate enough cash flow, you are in TROUBLE

I don’t know where you are in the buildout of your financial pyramid, but it is CRITICAL you calculate the cash flow generated each month by your investments. If you have several rental properties, you will be fine. But if you only have a savingsaccount, you are definitely in TROUBLE. Why? Because a savingsaccount at current interest rate of 0,11% can not generate 800 Euro per month for example.

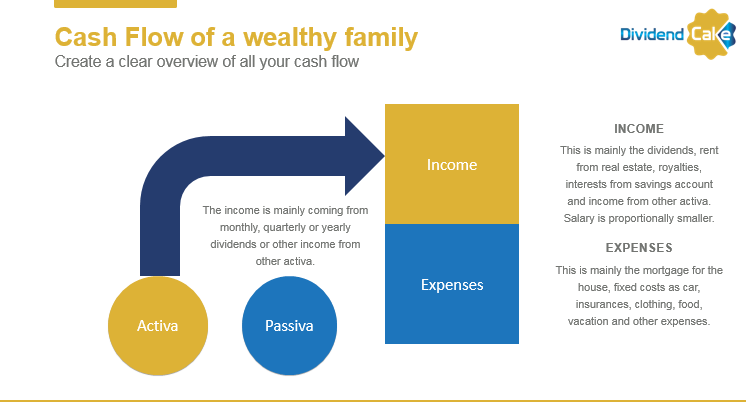

Here’s your home work. Calculate for all investments that you have what the cash flow is per month and per year. If you own a house, you could rent it out if you have good tenants. That is a possible option. Look at our Cash flow of a wealthy family that we describe in our Financial strategy.

A house is an asset and does not generate cash flow unless you rent it out. Your yearly rent income must be higher than all property taxes + maintenance costs, otherwise you lose money and you are cash flow negative.

Make sure you know your cash flow from your investments. A savingsaccount does not generate a MONTLHY INCOME.

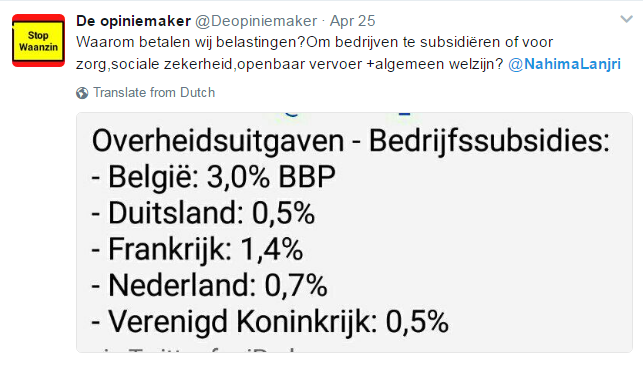

Conclusion 3 : Where did all our tax money go to?

Today government expenses are 3% of GBP. In other E uropean countries this is a lot lower. The government debt is still amongst the highest in Europe. We belong to the group of countries with large government debt such as Portugal and Greece. And the politicians keep on shifting the bill to future generations.

uropean countries this is a lot lower. The government debt is still amongst the highest in Europe. We belong to the group of countries with large government debt such as Portugal and Greece. And the politicians keep on shifting the bill to future generations.

Where does all money go to? People pay sometimes 50% or more taxes on their gross salary. In addition we have many more additional taxes such a financial stock market tax, dividend taxes of 30%,…almost everything has a tax !!

Belgian people keep on paying high taxes and you wonder where does all this money go to? How much money gets wasted ? Today each local city can manage their pension homes. When you read about the price differences of pension homes within different cities, why? Is the government using Business Analytics to put all costs together of all pension homes in Belgium and comparing the efficiencies and waste of each pension home ? It appears to me that pension homes are moving towards profit centers where deficits of local cities can be filled with. This is alarming…

Final conclusion

If you don’t prepare for your retirement, you will be in trouble. The difference between the cost of a pension home and your pension will need to be paid either from the cash flow of your investments or from the savings that you gathered over the years. Government expects you to pay the bill…

So let’s do quick math here…

Asssume that you need to go in a pension home at the age of 80 and you receive a pension of 1200 Euro. Thank God that you are healthy and don’t have major medical costs. You need to pay an additional 800 euro per month from your retirement savings. This is a cost of 9600 Euro per year. As life expectations are higher year after year, you can easily live until the age of 90 or more. That means that require at least a savingscapital of almost 100.000 Euro for a 10 year period. But the sad part is that you are consuming the capital that could be beneficial for your kids and your future generation…. so the government will make you completely BROKE and POOR if you don’t ACT and PLAN EARLY !

Even worse will your situation be when you don’t have the capital saved and the government will knock at the door of your kids to pay the bill? Then your kids become poorer….as well.

The proposal of this political party raises also other KEY THREE QUESTIONS ? I list them out..

- How will the government motivate people to save for their retirement in a climate of high taxes and life becoming more expensive due to inflation ?

- How will pension pay out evolve and increase over time to support the increasing costs of medical care ?

- How will the government keep pension homes affordable? Is the goal of a pension home to be a profit center or an efficient managed cost center ?

Personally I don’t have a problem to assist my mom financially but the key priority is to activate her sleeping capital to generate a cash flow that can support her future medical care and pension home WITHOUT consuming her savings and selling her house. I don’t want the government to make my mom poor.

Personally I consider the proposal of this political party horrific as there are so many other actions a government can take….instead of making families poor after paying years of high taxes.

PREPARE WELL FOR YOUR RETIREMENT AND ACT NOW !

DON’T ALLOW THE GOVERNMENT TO MAKE YOURSELF AND YOUR KIDS POOR !

INVEST WISELY AND CREATE THAT CASH FLOW TREE…

4 Response Comments

Spot on article.

That is quite a scary reality. For some reason the government always have their hands in the cookie jar.

It has always been the one fundamental flaw in the EU that it doesn’t have a centralized mechanism to control debt spending in all of it’s countries. Unfortunately that kills the ordinary citizen later down the road because there is no fiscal responsibility.

Hi John

I agree with you. EU institution does control governments budget but they are tolerant when it concerns lowering government debt. Europe can not dictate anything unless you need European money such as in the case of Greece. The fiscal responsibility remains a government’s responsibility and in Belgium politicians keep on pushing a budget in balance out to next years. Yesterday government sold a part of their shares of a French bank BNP Paribas and it will ONLY be a 0,5 % drop of government debt.