Belgian people are known within Europe as savings champions. In a survey about money at the end of March (see Blog post “Saving Belgian has no appetite for risk …Our reflection.” ) it was concluded that 67% of Belgians are saving money and 33% could not. The average amount is around 200 Euro.

But does that mean people have a financial buffer or an emergency fund in place ? Does that mean people have correctly sized their financial buffer ? Not really…15 % said they prefer to enjoy life and spend money. Today we reflect on how you should calculate your financial buffer, the layer 1 in our Financial Strategy. Do you need an emergency fund? How big should it be?

Our 3 main reasons for building a financial buffer ?

A happy life is for many people equal to a life without any big financial problems. But we all know the law of Murphy. No matter how financially prepared you are, life has a way of throwing curve balls that you never expect. Those “unexpected expenses” are the reason many financial professionals suggest keeping three to six months of expenses tucked away in a savings account or investment that is fairly easy to access.

Even if you can’t imagine a scenario where you would need rescuing, remember: anything can happen. Here, for example, are 3 situations where you might need a financial buffer for.

- Losing your job : Companies relocate to another country based on profit targets, older employees become too expensive, …many reasons exist why you can lose your job tomorrow. And you don’t see it coming… With an Emergency Fund you could live off of your savings while you search for the perfect position. Without an emergency fund, on the other hand, you could be forced to take the first job that comes along – whether you want to or not.

- Illness : Health is the most important asset we have in life. However you can become sick suddenly or your spouse or your child needs an urgent medical treatment. Even if you have health insurance, you may need to foot the bill for out-of-pocket costs until you reach your deductible.

- Other unexpected events : Many other unexpected events can occur. For example your car doesn’t start in the morning. Nothing is worse than a “surprise” car repair bill. One of your friends needs financial help. You find out that your partner is cheating on you and decide to move out of the apartment. A divorce is another event that leads to many unexpected costs. Owning a house also results in maintenance costs. Unexpected events always lead to unexpected costs.

But how big should your financial buffer be?

Never worries about money with the correct financial buffer ?

The size of your financial buffer or emergency fund depends on different elements, such as your living standards and the composition of your family. Are you single, married or living together? Do you rent or did you purchase a house? Do you own a car or do you use public transportation? Families with their own house need a bigger financial buffer than someone who lives in a rental flat or house. A house means more maintenance expenses. Someone who has a higher salary, better foresees a higher buffer as his expenses are most likely higher too.

Financial experts recommend to have a financial buffer which allows you to replace all your household equipment and/or your car. The minimum emergency fund that that you should have is the total amount of your two most expensive assets. For example your car and your washer machine.

The Dutch National Institute for Budget education, called Nibud, has made concrete figures about the size of a financial buffer. Singles (with a net salary of 1500 per month) should at least have 3.500 euro as financial buffer. A family that rents a house and has no kids, needs at least 4000 euro. A family with their own house and 2 kids, needs at least 5000 euro. Incredibly low, isn’t it? That’s what we think too as a replacement of a car costs at least 10.000 euro. Last year a newspaper listed a few examples of family situations with the adviced financial buffer. We list them out ranked by size.

- Millenial starting his first job : Net salary 1500 euro ; rent a flat ; no car -> Advice Financial Buffer : 3.500 euro

- Divorced lady with 1 child younger than 12 y old : Net salary 2600 euro ; own house ; lease car -> Advice Financial Buffer : 6.050 euro

- Single : Net salary 2000 euro ; rent a flat ; compact car -> Advice Financial Buffer : 12.300 euro

- Family with 2 teenager kids : Net salary 4000 euro ; own house ; Lease + compact car (10k) -> Advice Financial Buffer : 20.600 euro

- Family (30y old) without kids : Net salary : 5000 euro ; rent a house ; middle class car (15k) -> Advice Financial Buffer : 25.3500 euro

- Single Income family with three kids : Net salary : 2500 euro ; own house ; middle class car and second car -> Advice Financial Buffer : 31.800 euro

- Family (50y old) with 2 married kids : Net salary 6000 euro ; own house ; high class car (30k) -> Advice Financial Buffer : 44.050 euro

What do you think about those numbers ? How does it compare with your family situation ? Personally we think you need to build at least six months of salary as an emergency fund when you are young. Above that number, you can save in layer 2 (your retirement fund) or save for that dream in layer 3 of your financial pyramid. This could be a new car, travel to an exciting country, or the startup of your own company…you name it

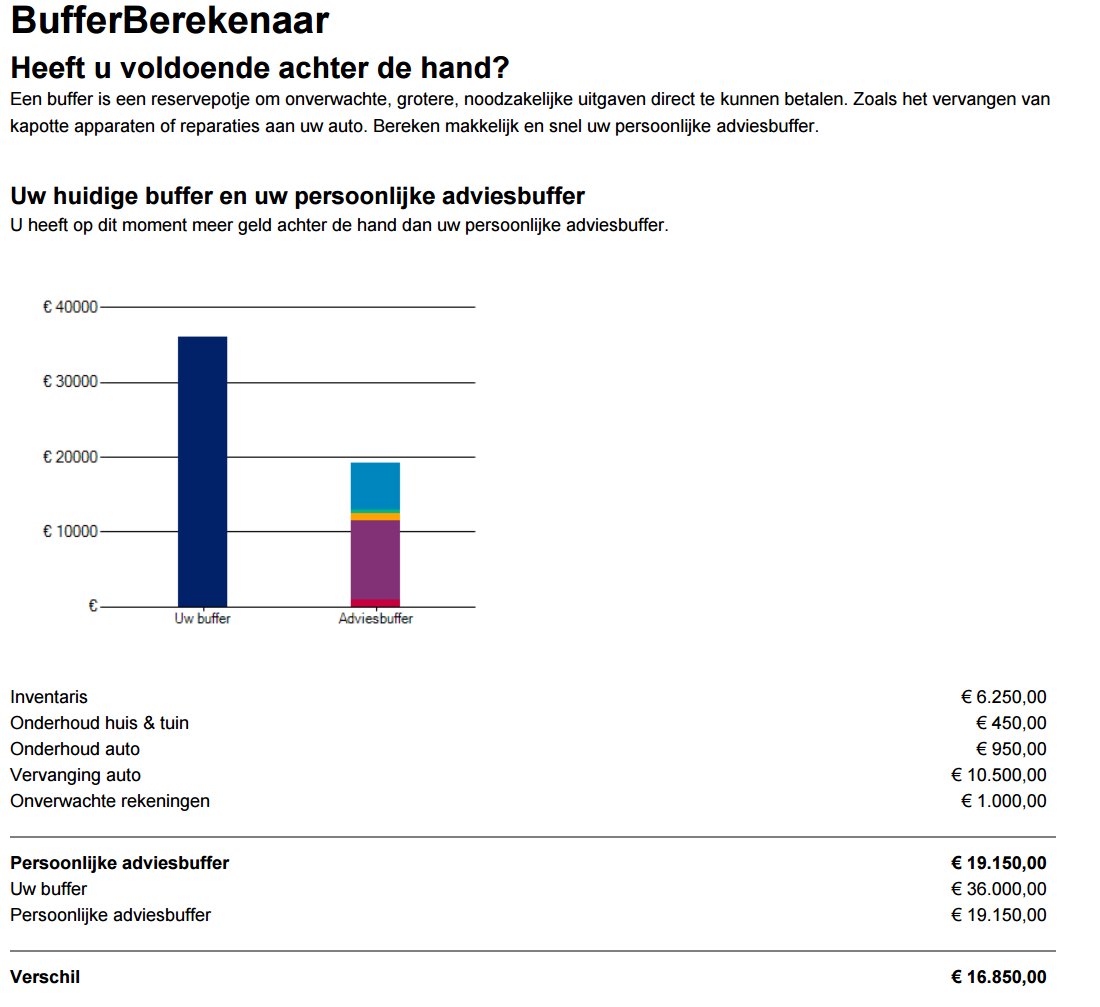

Do the Test and calculate the size of your Emergency Fund !

If you want to calculate your personal financial buffer, click on the below link :

This model gives you a good idea but can not foresee ALL unexpected expenses. So there’s no bucket for losing your job or your lease car for example. So we did run our numbers and current situation through this calculator. What did we learn ?

This model gives you a good idea but can not foresee ALL unexpected expenses. So there’s no bucket for losing your job or your lease car for example. So we did run our numbers and current situation through this calculator. What did we learn ?

- We have sufficient financial buffer. The minimum emergency fund is 19.150 Euro.

- As the financial calculator does not include job loss and the loss of our lease car, we believe that the additional buffer of 16.850 euro can cover any unexpected expenses as a result of such events.

- Going forward we may need to increase our financial buffer to 40k when our family situation changes.

As a saving account does not generate any cash flow, we try to limit any further additions to our savings account. Instead we focus on building and increasing our second passive income with our dividend investing strategy. We learn from above figures that it is important to grow your emergency fund from around 3500 euro (when you in your 20’s) towards 45000 euro when you are in your 50’s.

Always Be Positive

A few years ago when I was going through my divorce and as a result moving into a new house, buying new household and furniture, paying for a lawyer,…I was very happy that I had saved an emergency fund. I could complain about the loss of money but there is no point in getting upset when the inevitable happens. Carefully assess the situation and the damage. Try to understand how much it will cost you to remedy the situation and financial blow. If you don’t have the money to pay for it, think of how you can get there — whether it’s through “side hustling” or the generosity of a family member.

If you do have the money to pay for making yourself happy and deal with your financial issue, go ahead and do it, and don’t give it another thought. It’ll drive you crazy to think of everything else you could have done with that money. Instead, be grateful you were wise enough to save ahead of time and start preparing for the next financial blow! Always think positive !!

Have you ever had to pay for an unexpected financial blow? How did you deal with it? How is your size of your emergency fund ? Do you revise it on a periodic basis? What do you think about our emergency fund? Is it too big or too little? Let us know your comments and feedback

2 Response Comments

Interesting analysis overall, I guess this changes overall depending on cost of living and salaries received. Thanks for sharing

Just did the test… we are over the calculated buffer.

In order to sleep well at night, I prefer to have a higher buffer. On the other hand, as long as you have an income and save a decent amount of money, you could have a smaller buffer… I am still uncertain about the right size.

I think over time, it will reduce. especially when our tak21 reaches 8years and 1 day.