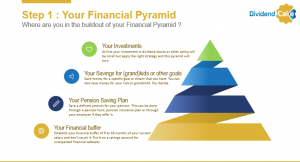

1. Invest in what you want

2. Put the money on a savings account

3. Start with a Pension Fund

4. Invest in a Investment Funds Plan

An alternative for a savings account is a investment fund plan. This allows you to invest on a monthly basis or per quarter. You can invest according your risk profile. For many investment plans you don’t need any knowledge or experience. You can start with 25 Euro per month. So with vacation money, you can start your investment plan for your kids or as an extra alternative for your savings account.

On the following link you can compare different investment plans from different banks.

5. Invest in Stocks or ETFs

If you have invested in all of the above, you can still chose to invest in a stock or a diversified sector, country of index ETF. Always look at the cost of mutual funds if you want to invest in them. Listen to the following podcast of Kirk DuPlessis of Optionalpha.

Hidden Mutual Fund Fees Are Killing Your Portfolio Growth Curve

I sometimes get people like my mom who are saying to me, “What about this mutual fund that was recommended by the bank ?” So, I think there are things that people don’t really consider when it comes to mutual funds that might help out. First things first, I don’t think that I’m actually totally shocked that people still invest in mutual funds because we know most mutual funds have higher expense ratios than say an ETF or an index fund. I think the average expense ratio is at least over 1% still for most mutual funds. At least that’s according to Morningstar right now. And that expense ratio can actually trim a lot of your nest egg. If you think about how money compounds and how just even a 1% difference, even though it doesn’t sound like a lot, actually can really dramatically trim how much money you have after 30 years of investing. In many cases, it could trim hundreds of thousands of dollars and you don’t even really realize it. Listen to the podcast and make yourself smarter !

Final Words : How do we invest our Vacation Money ?

How did we invest our vacation money ? We always take a percentage % approach for investing our vacation money. We invested in three pillars of our Financial pyramid. Here’s the % split of our investments :

1. Emergency Fund : We did add 12% of our vacation money into our Emergency Fund. As we are now a family of 5 people, I need to increase our emergency fund for future emergencies like health problems or kids’ studies. We did not add this money to our savings account but to our monthly investment fund plan.

1. Emergency Fund : We did add 12% of our vacation money into our Emergency Fund. As we are now a family of 5 people, I need to increase our emergency fund for future emergencies like health problems or kids’ studies. We did not add this money to our savings account but to our monthly investment fund plan.

2. Investing for specific goals : We did invest 27% in my wife’s driving classes. My wife does have a driver’s’ license. But Belgium does not acknowledge this license of her country, so she has to practice the exercises and road rules in Belgium. Then she can apply for a Belgian driver’s license.

We also invested 1% to start a monthly investment plan for one of the kids.

3. Our Vacation location : This year we are going on vacation to La Bella Italia. The first time we go as a family to Italy. We spend most of our vacations in France during past years. This year will be different. The remainder 60% of our vacation money will be put aside for the rent of our vacation home and money we need locally. We are looking forward to our vacation in one and half month.

We hope you learned something from this blog post and keep on following us on Twitter and Facebook. As always we end with a quote.

4 Response Comments

it’s so interesting you get a bonus titled vacation money. I guess it’s not strictly for vacation though if you invest it wisely. If I get something like this I would invest and only use passive income from it on vacation. so backyard camping in the first few years, culminating to an Antarctica cruise in my old age.

Thanks for the feedback. An Antarctica cruise seems appealing but I don’t think I will survive the cold at old age..wink 🙂

Or just go in a cheap holiday. We went in camping last years and we spend a part of the money from the 13th salary (not all, only 1500 euro) -but back at home at my excel budget I noticed we saved on energy for July, almost zero on fun budget, almost zero on the food budget, almost zero payment for summer activities for our child – 1000 not spend in July (comparing with august).

Bonus: no D vitamin supplements and great sport and health.

This year we will do it better 🙂

Well, its not really vacation money, is it? It is just your annual salary divided artificially by 13 and giving you an extra salary. In a way, a state imposed way of managing your finances!

I live in Austria, where the state goes even further, it divides the annual salary by 14 and makes sure its financially irresponsible citizen have money for vacation and Christmas presents.

By the way, is your recommendation 2 (savings account) serious? It implies a real loss on your money in Europe these days…

All the best and enjoy your vacation 😉

MFF